Venture capital has, for a long time, played an important role in the modern British economy. Over the past 50 years, it has funded young and promising businesses that went on to become future leaders of British industry.

The UK venture capital industry has been pivotal in the success of current national champions such as Deliveroo, Revolut, Brewdog, Monzo, Darktrace and Gousto, to name a few. All the while, it has done so while dwarfed – in capital terms – by its buyout market cousin.[1]

The Conservatives have long been at the cutting edge of supporting early stage business in the UK. In 1993 and 1995, the Major Government introduced the Enterprise Investment Scheme and Venture Capital Trusts, two revolutionary projects that have since allowed nearly 30,000 SMEs to benefit from over £20bn in investment capital.[2]

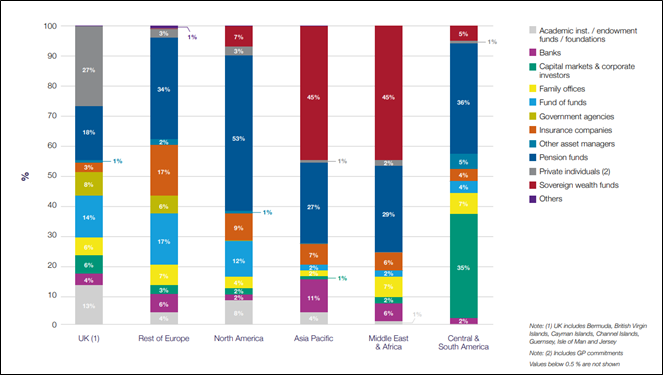

The BVCA’s latest Report on Investment Activity (2019 – below) showed the result of our SEIS, EIS and VCT schemes. When compared with other countries, a far larger proportion of UK capital comes from private individuals (who benefit from the EIS and VCT schemes) than in other countries – 27% in the UK compared with 3% in the US and EU.

This is positive, because it shows that early stage venture capital initiatives instigated by the Treasury are effective. Moreover, private individual capital is needed in the UK, as a major source of capital in other countries – pension funds – are materially more risk adverse in the UK than Europe or America.[3]

And while the Conservative’s track record in support of early stage UK business is strong, there is more to be done.

Later Stage Funding

Post-COVID, the most attractive way for us to reduce our Debt-GDP ratio and ensure prosperity for all is through ensuring UK industry grows and thrives – and does so at a rate faster than before Coronavirus hit.

To do this, the UK venture capital market must remain as flexible, buoyant and diverse as possible.

One area where the UK is falling behind is in late stage venture capital. Helped by projects such as the SEIS, EIS and VCT schemes, 2019 saw early stage investments increase 80% year-on-year to £865m, and start-up stage investments grow 79% to £210m. However later stage venture capital did not see the same gain. It grew just 39% in the same period, to £467m.[4]

At the same time, Venture Capital Trusts have been raising material capital. With its attractive 30% income tax relief for investors, the sector raised £716m in the 2018/9 tax year[5] – the second highest level in the market’s 24-year history – and £619m in the 2019/20 tax year, even as the first Coronavirus lockdown was taking hold.[6]

Tweaking the Rules

Despite the record VCT capital raised in past years, VCTs remain restricted in how they can invest. Where SEIS and EIS investors receive loss relief on their investments, VCT investors do not. This fact, combined with the lack of growth in UK late stage venture capital funding, begs the question why VCT capital is not being used to improve the UK’s later stage funding gap.

Here, the Conservative Government can unlock VCT capital and boost the UK’s later stage funding market by making just three changes to the VCT rules.

First, the VCT gross assets test threshold should be increased to £50m. At present, the gross assets of a company raising VCT capital, immediately before the fund raise, must be no more than £15m. After the fund raise, gross assets must be no greater than £16m. In practice, this rule prevents companies from raising later stage funding through VCT capital, as late stage funding rounds are frequently over £15m in quantum. By increasing the gross assets test threshold to £50m, it would ensure that VCT capital can be put to work efficiently in the UK’s late stage funding market.

Second, the maximum number of employees a company can have upon receiving VCT capital should be increased. At present, a company with more than 250 full time equivalent employees cannot receive VCT capital. This threshold should be raised to at least 500 FTEs, to ensure that businesses that employee British employees are not penalised from a VCT perspective. Shouldn’t we be incentivising companies to employ as many British staff as they reasonably require?

Third, if and when permitted by state aid rules, the limit on total VCT funding received by a company should be increased, from its current limit of £12-20m, to £75m. Doing this will ensure that companies can raise late stage VCT capital, and remain comfortably within the fund raising limit.

With these three simple changes, the Conservative Government can unlock VCT capital and help the UK’s late stage funding market. It would turbo-charge the British economy, right when the country needs it.

[1] Buyout firms raised £41bn of new capital in 2019

[3] This is partly due to UK pension scheme rules, and partly cultural.

[4] BVCA Report on Investment Activity 2019 here